From slowdown to stabilization: global retail trends in Consumer Technology and Durables

June 16, 2023

Based on a new partnership between GfK SE, gfu Consumer & Home Electronics GmbH and IFA Management GmbH, we provide regular information on market developments and trends in the consumer electronics and home appliances industry. Interesting insights, current market figures, consumer trends and much more will be professionally prepared for you from the sources of the three expert partners.

After two years of pandemic-driven “cocooning” driving growth for consumer goods, the sector is now facing several challenges.

Various factors have influenced consumer behaviour in recent years. The most significant are rising food prices, energy supplies, and fuel — commonly referred to as a cost-of-living crisis. This has led to stagnation in real incomes and, together with the war in Ukraine — which was also a cause — has dampened consumer sentiment.

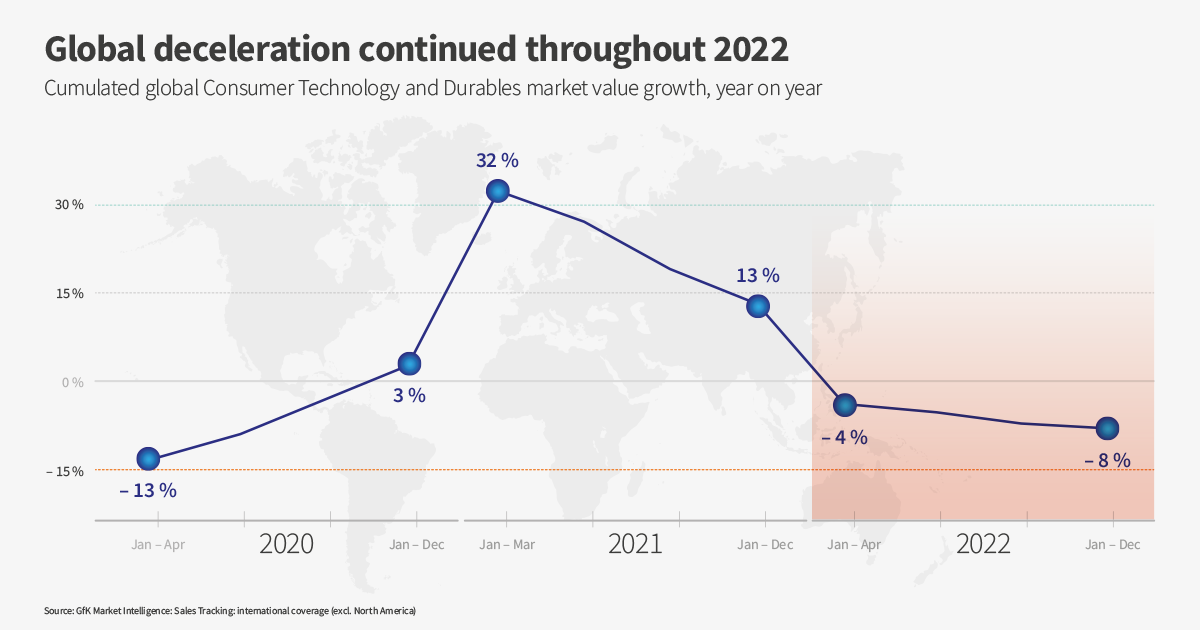

At the same time, large parts of the market are also still saturated after consumers pushed forward both major and minor purchases in the domestic sector during the pandemic. After the peak sales in 2020 and 2021, the full year growth for tech and durables sectors declined by -8.4 % in value growth in full year 2022.1 Growth perspectives are therefore to be estimated as challenging within the next 12 months for manufacturers and retailers. The market is forecasted to be stabilizing at low levels with value growth dynamic -0.4 % in 2023 versus previous year. 2

Turning the trend around?

However, there are early indicators of positive change on the horizon, with some regions benefiting from a gradual stabilization in consumer prices and a minor easing of inflationary pressures in December 2022. This has led to differing economic forecasts for 2023 — depending on the region, of course.

As per chief economist survey in January of 2023, in Europe, 100% of chief economists predict weak economic growth, while 91% do so for the United States. That contrasts sharply with South Asia, where only 15% of economists predict weak growth, and the Middle East and North Africa, where 30% do so.

What does this mean for brands?

“There is no doubt that tech manufacturers and retailers are facing a period of significant challenges. Nevertheless, there are numerous opportunities where they can seize growth by relying on insight-led strategies. For example — brands should expect the strongest demand to arise from the ‚affordable premium‘ tier, as consumers balance their new price-sensitivity against their demand for products that offer increased levels of user convenience, performance and sustainability. This trend will be particularly apparent during key promotional periods for the technology industry.“

Jan Lorbach, Senior Director Strategic Insights at GfK

Sources

GfK Market Intelligence: Sales Tracking: international coverage (excl. North America); sales value growth percentage in USD; initial 2020 cumulated period spans Jan-Apr to include the outbreak and first lockdown of COVID

1 GfK Global Panelmarket tracking excluding North America, Sales Value Growth, USD non-subsidized pricing

2 GfK International coverage extrapolated including North America, Sales Value Growth, USD non-subsidized pricing, forecast on February 22, 2023

If you want to stay up-to-date with the latest developments in tech and what's happening with IFA, subscribe to our newsletter here.